Key Takeaways

- The 30-year fixed mortgage rate is currently sitting at approximately 6.43 percent, a six-month high, driven by oil market disruption from the ongoing US-Israel-Iran conflict that began February 28, 2026.

- The Federal Reserve held rates steady at its March 17 to 18 meeting and now projects only one 0.25 percent cut for all of 2026. Waiting for the Fed to rescue your mortgage rate is not a strategy the data supports.

- DFW buyers currently have access to nearly 40 percent more inventory than a year ago, homes averaging 65 days on market, and seller concessions in roughly half of all active transactions.

- The payment difference between today's 6.43 percent rate and last fall's 5.75 percent rate on a $360,000 loan is approximately $160 per month. That gap can be closed entirely through a properly structured rate buydown.

- Builder incentives in submarkets like Frisco, Prosper, Celina, McKinney, and Mansfield are currently running $15,000 to $30,000, with buydowns of 100 to 200 basis points available.

The Transmission Chain: How a War 7,000 Miles Away Moves Your Rate

Most buyers understand mortgage rates in only one direction: up or down. What they rarely understand is the mechanism, the precise chain of events that transmits a military conflict in the Persian Gulf into a higher number on their monthly mortgage statement. Understanding that chain changes how you make decisions.

On February 28, 2026, the United States and Israel launched joint strikes on Iran. As of late March 2026, that conflict is in its fourth week with no clear resolution on the horizon. Iran's Islamic Revolutionary Guard Corps responded by effectively closing the Strait of Hormuz to international shipping traffic. According to the International Maritime Organization, more than 3,000 vessels are currently stranded, and tanker traffic through the strait has dropped approximately 70 percent from pre-conflict levels.

The significance of the Strait of Hormuz is almost impossible to overstate. According to the U.S. Energy Information Administration, the strait carries roughly 20 percent of global petroleum liquids consumption and more than a quarter of all seaborne oil trade. It is the single most important chokepoint in the global energy supply chain. When it functionally closes, the price of oil moves fast.

Brent crude, which was trading near $70 per barrel in early February, shot past $112 following the conflict's escalation. The International Energy Agency responded by coordinating a record release of 400 million barrels from strategic reserves, an extraordinary intervention designed to stabilize markets. As of late March 2026, the Trump administration announced a temporary lifting of sanctions on Iranian oil loaded at sea through April 19, which pulled prices back to approximately $100 per barrel. The IEA release and the sanctions relief have provided some floor, but oil at $100 per barrel remains meaningfully higher than it was six weeks ago.

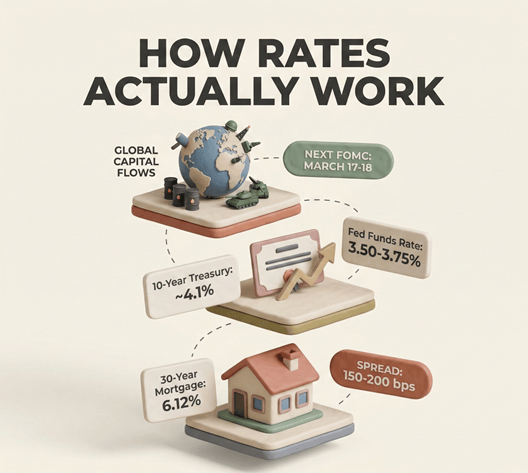

Here is where the mortgage connection becomes explicit. Mortgage rates are not set by the Federal Reserve. They are priced off the 10-year U.S. Treasury yield, the benchmark that reflects investor expectations about inflation and economic stability over the next decade. When investors believe inflation is rising, or will rise, they demand a higher return to hold long-dated bonds. They sell bonds. Bond prices fall. Yields rise. And when the 10-year Treasury yield rises, mortgage rates follow within days.

As of the week of March 24, 2026, the 10-year Treasury yield is sitting at approximately 4.37 to 4.39 percent, a 7.5-month high, up from around 4.1 percent in early March. The 30-year fixed mortgage rate has tracked from the high 5 percent range in late 2025, through roughly 6.1 percent in early March when tensions first escalated, to its current level of approximately 6.43 percent.

The chain is this: oil disruption drives inflation fear, which triggers a bond selloff, which pushes Treasury yields higher, which raises mortgage rates. It is not mysterious. It is mechanical. And it is the reason your mortgage rate is being influenced by a conflict on the other side of the planet.

Where the Fed Stands: A Hawkish Pause with No Rescue in Sight

Understanding the Federal Reserve's position matters enormously right now, because a significant number of buyers are making decisions based on an assumption about the Fed that the data does not support.

The Federal Open Market Committee met on March 17th and 18th, 2026. They held the federal funds rate steady at 3.50 to 3.75 percent, which was universally expected. What was not universally anticipated was the clarity of Chair Jerome Powell's language at the subsequent press conference.

Powell stated directly: "The net of the oil shock will still be some downward pressure on spending and employment and upward pressure on inflation." He added that the Fed's forecast shows it "will be making progress on inflation, not as much as we had hoped." These are not the words of a central bank preparing to cut rates. They are the words of a central bank in a genuine policy bind: an oil shock that simultaneously raises inflation and threatens growth, the classic stagflationary pressure that limits the Fed's ability to cut without making inflation worse.

The revised dot plot from the March meeting projects a single 0.25 percent cut in all of 2026, followed by one additional cut in 2027. The Fed also revised its 2026 inflation forecast upward, from 2.5 percent in December to 2.7 percent.

For context: the official February Consumer Price Index came in at 2.4 percent year-over-year, released on March 11th, before the full price impact of $100-plus oil had filtered through to consumer goods, logistics, and food. March CPI will not be released until April 10th. Most economists expect the March figure to be higher. That means the next data point the bond market is watching will likely push inflation expectations further, not pull them back.

The picture the Fed is painting is one in which mortgage rates do not fall materially in 2026. One quarter-point cut to the federal funds rate (which does not directly move mortgage rates anyway) is not the catalyst that brings the 30-year fixed back to the mid-5s. If you have been waiting for the Fed to ride to the rescue, this is the moment to update that assumption.

The DFW Buyer's Actual Position Right Now

Here is where the national narrative diverges from the local reality, and the divergence matters.

The national coverage of the mortgage rate environment is accurate as a general statement: rates are elevated, affordability is under pressure, and buyer sentiment is cautious. What that coverage almost never addresses is what any of it means in a specific market at a specific moment in time. Dallas in late March 2026 is not Phoenix. It is not Austin. And it is not the Dallas of 2021.

According to data from HBI Blog and multiple DFW market trackers, active listings across the DFW metro are up approximately 40 percent year-over-year, with close to 30,000 active listings at any given point. Homes are averaging 65 days on the market, up from around 45 days a year ago. That is not a typo. Homes are sitting for more than two months on average before going under contract.

Roughly 50 percent of all active transactions in DFW currently include some form of seller concession: closing cost credits, repair allowances, interest rate buydowns, or some combination. That figure is consistent across multiple DFW brokerage data sets and reflects a market where sellers have adjusted to the new reality even if buyers have not fully caught up.

Median home prices across the DFW metro sit in the $385,000 to $420,000 range depending on the data source and geographic boundary. Values did soften approximately 5 percent through 2025, according to M&D Real Estate's year-end market recap. They have not crashed. The market is not distressed. But the balance of power between buyers and sellers has shifted in a way that is unmistakable at the transaction level.

It is also important to understand what the phrase "DFW market" actually means in practice. The metro is a collection of micro-markets that behave independently. Frisco, Prosper, and Celina look nothing like Lakewood or East Dallas. Some suburban corridors have 90-plus days of supply on specific product types. Others remain competitive. The data points above are metropolitan averages. Your experience will depend entirely on your target area, price range, and product type. But across the board, this is one of the most favorable buyer environments DFW has produced since before 2020.

Those are the conditions on the ground right now. Whether they work in your favor depends on your specific situation, timeline, and target area.

The Real Cost of the Rate Environment

Understanding what today's rates actually mean in dollar terms is important for anyone evaluating whether to buy, wait, or stay on the sidelines.

On a $400,000 home purchase with 10 percent down, a $360,000 loan at today's rate of 6.43 percent generates a monthly principal and interest payment of approximately $2,260. At 5.75 percent (where rates were in the fall of 2025), that same $360,000 loan generates a payment of approximately $2,100. The difference is roughly $160 per month.

That $160 is real. But it is also not the only variable in the calculation.

Market conditions shift alongside rates. If rates eventually fall, it is reasonable to expect that inventory will tighten, seller concessions will decrease, and competition will increase, all of which affect the final price and terms of a transaction. Conversely, if rates stay elevated or rise further, the current inventory and concession environment may persist longer.

The point is not that one path is better than the other. The point is that rate alone does not determine cost. The total cost of a home purchase is a function of four variables: the asset price, the interest rate, the market conditions at the time of purchase, and the resulting monthly payment. Evaluating any one of those in isolation, particularly the rate, produces an incomplete picture.

Understanding Rate Buydowns: How They Work

One of the tools available in the current market is a rate buydown, a mechanism that reduces your effective interest rate, either temporarily or permanently. In the current DFW environment, buydowns are available through two channels.

Track One: Resale Seller Concessions

With roughly 50 percent of resale transactions in DFW currently including some form of seller concession, there is genuine room in many negotiations to ask for a seller-paid rate buydown as part of the contract. This is not a novel request. It is a standard term that experienced agents negotiate regularly. The structure is straightforward: instead of a closing cost credit or a price reduction, you ask the seller to contribute funds to the lender at closing to buy down your interest rate.

A 1-point permanent buydown, meaning the seller pays approximately 1 percent of the loan amount to the lender at closing, typically reduces your interest rate by approximately 0.25 percent for the life of the loan. On a $360,000 loan, that is $3,600 from the seller's side of the transaction, and it takes your rate from 6.43 percent down to approximately 6.18 percent. Your monthly payment drops by roughly $55 to $60 per month. The breakeven on that concession is approximately five years, assuming you never refinance. If rates improve and you refinance in two or three years, you received the full benefit of the lower rate for the period you held the loan at that level.

A more aggressive version, a 2-point permanent buydown, costs the seller approximately $7,200 on that same loan and takes your rate to approximately 5.93 percent. Monthly payment on that loan is approximately $2,140, which is within $40 of where you would have been if you had purchased last fall at 5.75 percent. The seller is funding the difference.

Track Two: New Construction Builder Incentives

The second track requires a different conversation but often produces even more significant rate relief. Builders in the northern DFW growth corridors (specifically Frisco, Prosper, Celina, McKinney, and Mansfield) are currently offering rate buydowns of 100 to 200 basis points backed by incentive packages of $15,000 to $30,000. These are not hypothetical. They are the standard competitive offering in those markets right now, and they reflect a builder environment where inventory has accumulated and sales velocity has slowed from its peak.

A 2-1 temporary buydown, one of the most common builder structures, reduces your effective rate by 2 percent in Year 1 and 1 percent in Year 2, with the full contracted rate applying from Year 3 forward. At today's 6.43 percent rate, a 2-1 buydown puts your effective Year 1 rate at approximately 4.43 percent and your Year 2 rate at approximately 5.43 percent. Year 3 and beyond, you are at 6.43, or if rates have improved and you refinance, potentially lower.

The Year 1 payment on a $360,000 loan at 4.43 percent is approximately $1,802 per month. That is a $458 monthly difference compared to the unmodified rate. On an annual basis, that is nearly $5,500 in payment relief during your first year in the home.

There are important caveats with builder incentives. Builders who offer large buydowns often require buyers to use their preferred in-house lender, whose rate on the base loan (before the buydown) may not be the most competitive available. The incentive on the buydown can be partially or fully offset by a less favorable base rate. The only way to evaluate a builder incentive properly is to model the full loan package side by side with an independent lender's offer. A good buyer's agent will run this analysis as a standard part of the representation.

The broader point is that rate buydowns are a standard tool in real estate transactions, and in the current DFW environment, the conditions exist for them to be negotiated more frequently than in a tighter market. Whether a buydown makes sense depends entirely on your holding period, your refinance expectations, and the specifics of your deal.

Frequently Asked Questions

Q: If I buy now and rates fall significantly in the next year or two, can I refinance?

Yes, and this is an important part of the calculus. Refinancing is available to any homeowner who qualifies at the time of the refinance, and there are no prepayment penalties on standard conventional loans. The practical decision framework is this: if you buy today at 6.43 percent with a seller-paid buydown reducing your effective rate to 6.18 percent, and rates fall to 5.5 percent in 2027, you refinance. Your holding cost during the higher-rate period is the delta between what you paid and what the new rate would have been, which was partially offset by the buydown you negotiated into the deal. Homeowners who bought at 7.5 percent in 2023 are refinancing today. The same cycle will recur.

Q: How do I know if a seller concession for a rate buydown makes more sense than a price reduction?

The answer depends on your holding period and your financing structure. A price reduction lowers your principal balance and therefore your monthly payment by a small amount permanently. A rate buydown on the same dollar amount produces a larger monthly payment reduction but is only present while you hold the original loan. If you plan to hold the property for more than five to seven years and not refinance, a price reduction may produce more total savings. For buyers who expect to refinance within three to five years as rates improve, a buydown typically wins on total cost during the holding period. Your lender can model both scenarios side by side in about ten minutes.

Q: Is the DFW market actually in buyer's territory everywhere, or just certain areas?

Selective buyer advantage is more accurate. The metro-wide averages (40 percent more inventory, 65 days on market, 50 percent concession rate) are real, but they mask significant variation by submarket, price range, and product type. At price points under $350,000 in well-located areas, the market remains more competitive because demand at affordable price points has held. In the $400,000 to $700,000 range across the suburban growth corridors, buyer leverage is strongest and inventory is most plentiful. Above $1 million, the market is more property-specific and depends heavily on neighborhood and condition. The practical takeaway: do not assume you have leverage everywhere, and do not assume you lack it anywhere. Get a micro-market read before you decide how aggressively to negotiate.

Q: What is the risk of rates going higher from here?

It is real, not theoretical. The March CPI report, due April 10th, is expected to reflect higher prices than February's 2.4 percent figure. The full oil price impact had not yet been captured in the February data. A March CPI print above 3 percent would likely push the 10-year Treasury higher, and mortgage rates would follow. Rates at 6.7 or 6.8 percent are within the range of plausible outcomes by late spring if the oil shock proves more persistent than current futures markets expect. This is not a prediction. It is a scenario that the data does not rule out. Buyers who lock rates as part of a purchase contract before the April 10th release remove that uncertainty from their decision.

Q: What happens to DFW prices if this situation persists and rates stay elevated?

The most likely scenario for DFW is continued gradual softening, not a crash, but additional modest price normalization in the more overextended suburban submarkets. The city's fundamental demand drivers (employment growth, population migration, corporate relocations) have not reversed. But affordability constraint is real and eventually limits price. The more inventory accumulates, the more seller negotiating leverage erodes. For buyers, a prolonged elevated-rate environment is a mixed signal: it keeps rates high, but it also extends the favorable inventory and concession environment longer. If prices softened another 3 to 5 percent while rates stayed near 6.4 percent, the monthly payment on the same home would actually improve by more than a rate reduction of the same magnitude would produce.

Conclusion

This is a serious geopolitical situation with real financial consequences for American homebuyers. An active military conflict has disrupted the global energy supply chain, pushed inflation expectations higher, and moved bond yields to a 7.5-month peak. The Federal Reserve has signaled through its updated forecasts and Chair Powell's language that the path back to lower rates is narrow and slow: one cut projected for all of 2026, with inflation tracking above forecast.

For DFW specifically, the rate environment exists alongside a set of local market conditions (elevated inventory, longer days on market, widespread seller concessions, and active builder incentive programs) that are worth understanding regardless of whether you decide to buy now, later, or not at all.

The most important thing any buyer can do in this environment is understand the full picture: the geopolitical forces moving rates, the Fed's actual posture, and the local market dynamics in the specific submarket where they are looking. Rate alone does not tell the story. Neither does any single headline.

If you have questions about how these conditions apply to your specific situation, our team at Paragon Realty Advisors is available to walk through the numbers with you: the payment math, the buydown mechanics, and the micro-market conditions in your target neighborhoods.

Call or text us at (469) 290-7593 or visit paragondfw.com/contact.

Related Articles

New Construction vs. Resale in DFW: A Buyer's Decision Framework for 2026

How to Protest Your Property Taxes in Texas: The 2026 Playbook

The 2026 World Cup in DFW: What It Really Means for Real Estate

*Published by Paragon Realty Advisors | Uptown Dallas | paragondfw.com | (469) 290-7593*

*Data current as of March 24 to 25, 2026. Sources: Bankrate, BLS, Federal Reserve, EIA, IMO, IEA, CNBC, HBI Blog, M&D Real Estate, Realtor.com.*