Key Takeaways

- Builder incentives in DFW range from $10,000 to $50,000 — but they are negotiation tools, not gifts, and almost always come with trade-offs in loan terms, lender choice, or base pricing.

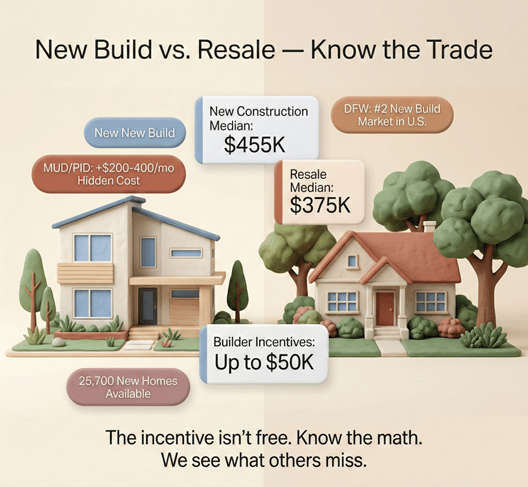

- The $80,000 median price gap between new construction ($455K) and resale ($375K) narrows significantly on a monthly payment basis once rate buydowns and closing cost credits are factored in — but MUD and PID taxes can add $200–$400 per month that never appears in the advertised price.

- DFW is the second-largest new construction market in the nation with over 25,700 new homes available from 188 builders — giving buyers more leverage and more choices than almost any other metro.

- Choosing new construction based on the shiniest incentive rather than the right location, tax district, and long-term cost structure is the most expensive mistake DFW buyers make.

- Independent inspections are non-negotiable for new builds — new does not mean flawless, and a builder warranty is not a substitute for a professional quality control process.

The New Construction Landscape in Dallas-Fort Worth

If you have been shopping for a home in DFW, you have seen the headlines: "Huge incentives! Rate buydowns! Closing costs covered!" On the surface, it looks like builders are handing out free money. They are not. Builder incentives are a trade — and if you do not understand the trade, you can end up overpaying, buying in the wrong location, or locking into a deal structure that costs more than it saves.

Dallas-Fort Worth ranks second in the nation for new construction building permits, trailing only Houston, with over 9,800 permits issued in just the first two months of 2025 alone. As of early 2026, approximately 25,700 newly built homes are available across the metroplex from 188 active developers. Annual new construction starts are projected in the 40,000–45,000-unit range, with closings expected to rise 15–16% year over year.

Meanwhile, the resale market remains constrained by the lock-in effect — homeowners sitting on 2.5%–4% mortgage rates are reluctant to sell, throttling existing inventory. The result: new construction now represents a disproportionate share of what is actually available to buy. That makes this comparison not just academic — it is the decision most DFW buyers will face in 2026.

This guide breaks down the incentive menu, the hidden costs, and the decision framework that separates a smart new construction purchase from an expensive one.

The Incentive Menu: Four Buckets Every Buyer Should Understand

Builder incentives in DFW typically fall into four categories. Understanding which bucket an incentive comes from — and what the builder gets in return — is the foundation of smart negotiation.

Bucket 1: Rate Buydowns

Rate buydowns attack the number buyers feel most: the monthly payment. The most common structure in DFW is a 2-1 buydown, which lowers the mortgage rate by 2 percentage points in Year 1 and 1 point in Year 2 before reverting to the note rate in Year 3. Some builders go further — Beazer Homes is currently offering a stepped four-year buydown at 1.99% / 2.99% / 3.99% / 4.99% for Years 1 through 4.

The distinction that matters: a temporary buydown is payment relief, not permanent savings. You are betting that your income rises, you refinance, or you are comfortable when the payment resets. A permanent buydown — paying points to reduce the rate for the life of the loan — can be powerful if you hold the home long enough to break even on the points.

The Paragon framework: do not accept a buydown because it looks good in the flyer. Accept it because the math works for your likely ownership horizon.

Bucket 2: Closing Cost Credits

Closing cost credits are the most straightforward incentive — cash toward title, lender fees, prepaids, and escrow. In DFW, builders are currently offering $10,000 to $30,000 in flex cash, with some spec homes carrying combined incentive packages up to $50,000. Highland Homes, for example, is advertising up to $50,000 in "Your Way" flex credits on select inventory.

The catch: these credits are almost always contingent on using the builder’s preferred lender. That is not automatically a bad deal, but it requires a side-by-side comparison — Option A with the builder lender and incentive versus Option B with an outside lender and no incentive. Compare cash to close, monthly payment, and total loan cost over your expected hold period.

Bucket 3: Design Center Credits

"Free upgrades" is one of the most effective marketing phrases in real estate. But most buyers do not realize how the design center works. Builders price the base home to look attractive, then the real house you want is created through packages and upgrades — flooring, countertops, lighting, appliance packages, extended patios, structural options.

The incentive may be pushing you toward a certain package tier, or it may be a credit that feels significant but still leaves a climb to your actual wish list. Buyers routinely spend $20,000–$40,000 more than planned when everything looks "only a little more."

The Paragon framework: set a hard budget ceiling before you walk into the design center. Prioritize structural options and livability upgrades — they hold value at resale. Hyper-custom finishes rarely return their cost.

Bucket 4: Price Reductions

Sometimes builders lower the base price, offer lot specials, or quietly adjust package pricing. This is the incentive builders resist most, because base price becomes a comparable sale for every other home they are trying to sell in the community. Builders would rather offer a $30,000 credit than a $30,000 price reduction — even though the economic impact to the buyer is similar — because the credit does not depress future comps.

Understanding this dynamic is leverage. If a builder has spec inventory that has been sitting, price flexibility is highest. Quick move-in homes carry real carrying costs, and builders are more motivated to negotiate on those than on ground-up builds with a six-month timeline.

The Hidden Cost Stack: What Never Appears on the Flyer

This is where payment shock happens. In DFW, new construction communities can carry a meaningful monthly cost stack beyond the mortgage that fundamentally changes the economics of the purchase.

MUD and PID Taxes

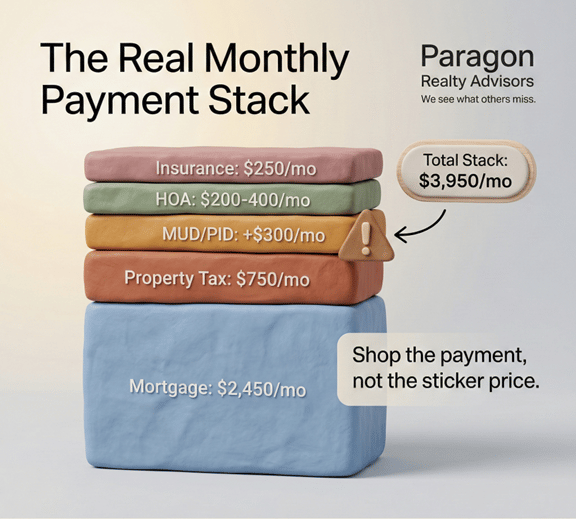

Municipal Utility Districts (MUDs) and Public Improvement Districts (PIDs) are special taxing districts that fund infrastructure and amenities in new communities. MUD tax rates in DFW typically run $0.70 to $1.40 per $100 of assessed value. On a $450,000 home with a MUD rate of $0.80 per $100, that is $3,600 per year — $300 per month added to your escrow that does not appear in the base price or the incentive headline.

PIDs fund neighborhood amenities like pools, parks, and trails, with typical fixed annual assessments adding another $175 per month. PID terms usually run 20–40 years, and homeowners can sometimes pay off their share in a lump sum. Combined, MUD and PID obligations can add $200 to $400 per month to a mortgage payment.

As of 2026, TREC Form 59-0 requires mandatory disclosure of special tax district obligations — but that disclosure often arrives after emotional commitment to a community. The smart move is to ask for the total effective tax rate before your first model home tour.

One cost that catches nearly every new construction buyer off guard: property tax assessment lag. In year one, the county taxes the property based on the unimproved land value, which keeps the initial escrow payment deceptively low. In year two, the full improved value — the house — hits the tax rolls, and the escrow adjustment can add hundreds of dollars per month overnight. Budget for the year-two tax bill from the start, not the year-one estimate.

HOA Fees

HOAs are nearly universal in DFW new construction. Standard single-family subdivisions run $55 to $160 per month. Master-planned communities with pools, fitness centers, and trails range $200 to $400 per month. Premium communities in Frisco, Prosper, and Southlake can exceed $400 per month. And HOA fees increase 3–6% annually as maintenance, insurance, and contractor costs rise.

The Paragon Payment Framework

Always underwrite your payment with realistic taxes, MUD/PID, HOA, and insurance included. A slightly cheaper house with higher tax and HOA obligations can cost more monthly than a higher-priced home in a different tax district. On a $450,000 new build in a MUD/PID community with a master-planned HOA, the total monthly stack — mortgage, taxes, MUD, PID, HOA, and insurance — can reach $3,800 to $4,200. That is the number that matters, not the base price.

Builder Contracts, Timelines, and Leverage

Buying new construction is not the same transaction as buying resale. With new construction, you are typically signing a builder’s contract — not the standard TREC resale contract buyers are accustomed to. Builder contracts are drafted by the builder’s attorneys and tend to favor the builder on key provisions: completion timelines can shift, certain allowances are builder-controlled, and deposit refundability varies by builder and phase.

Your leverage varies depending on demand. When a builder has spec inventory sitting — especially quick move-in homes that carry real carrying costs — negotiation room increases. The key signal: inventory age. A spec home that has been complete for 60+ days is a carrying cost the builder wants to eliminate.

The Paragon framework: treat the contract like a business deal. Know your deadlines, understand what happens if closing is delayed, understand what is refundable and what is not, and never assume "it will probably be fine" is a strategy.

Appraisals, Inspections, and the Quality Question

The Appraisal Risk in New Communities

Buyers often assume new homes always appraise. Not always. In a brand-new community, comparable sales can be thin or fast-moving. Builders protect base pricing aggressively, which means incentives can mask the true market clearing price. Appraisers evaluate closed sales and adjustments — not marketing language.

The risk is highest when you are paying a premium for a lot, for upgrades, or for a package above recent closings in the same community — especially when a community is transitioning from early-phase to later-phase pricing.

Why Inspections Are Non-Negotiable

New does not mean perfect. It means new. A builder warranty is valuable, but it is not a substitute for independent inspections. Best practice for new construction in DFW:

One DFW-specific reality that applies equally to new and existing homes: North Texas expansive clay soil requires active foundation maintenance from day one. A new build needs a sprinkler system and consistent perimeter watering just as much as a 1980s home. New does not mean immune to foundation movement.

Pre-drywall inspection — your only chance to see framing, electrical, plumbing, and HVAC before walls are sealed

Final inspection before closing — a comprehensive evaluation of the finished home

11-month warranty inspection — a professional walkthrough before your one-year builder warranty expires

One data point worth noting: Highland Homes reduced its structural and foundation warranty from 10 years to 6 years effective January 1, 2026. Warranty terms are not static — verify current coverage before you sign.

The Paragon Playbook: How to Buy New Construction the Smart Way

Whether you are a first-time buyer drawn to builder incentives or a move-up buyer comparing your options, this six-step framework turns the new construction decision from emotional to analytical.

Step 1: Choose your corridor and lifestyle first.

Do not let incentives lure you into the wrong commute or the wrong version of Dallas. A $30,000 credit in Forney does not help if your life revolves around Uptown.

Part of that corridor decision is the lot itself. New construction in DFW is increasingly built on 40 to 50-foot-wide lots, while resale homes from the 1990s and earlier often sit on a quarter acre or more. If outdoor space matters to your family, this is a meaningful tradeoff that no incentive package can offset.

Step 2: Underwrite the real monthly payment.

Mortgage plus property taxes plus MUD/PID plus HOA plus insurance. This is the number that determines your quality of life — not the list price, not the incentive headline.

Step 3: Treat incentives as a negotiation tool, not a gift.

Ask: rate buydown versus closing cost credit versus price reduction versus design upgrades — which one improves your specific financial outcome the most? The answer depends on your hold period, cash position, and financing structure.

Step 4: Lock your upgrade budget before the design center.

Prioritize structural and livability options first — garage extensions, covered patios, energy-efficient upgrades. These hold value at resale. Decorative finishes rarely return their cost.

Step 5: Confirm the comp story.

What has closed in the community? What is pending? What was included? Understand whether you are buying at, below, or above the established price point.

Step 6: Inspect everything.

Pre-drywall, final, and 11-month warranty inspection. This is not an insult to the builder. It is due diligence on the largest purchase of your life.

Frequently Asked Questions

Are builder incentives worth it?

They can be — if you understand the trade. An incentive tied to a preferred lender with unfavorable terms can cost more over the life of the loan than it saves upfront. Always compare the full cost of the deal, not just the credit amount.

Should I always use the builder’s lender?

Not always. Compare two scenarios side by side: the builder lender with the incentive versus an outside lender without it. Look at cash to close, monthly payment, and total interest cost over your expected hold period.

What is the biggest new construction mistake in DFW?

Choosing the wrong location because the incentive was compelling. A $50,000 credit in a high-MUD community 45 minutes from your office is not a bargain — it is a lifestyle and financial trap that compounds over time.

Are design center upgrades worth the cost?

Some are. Structural options, energy efficiency upgrades, and livability improvements hold value. Trendy finishes and hyper-custom selections rarely return their cost at resale.

Do I need an inspection on a new build?

Yes. New means new — not flawless. Pre-drywall catches issues before they are sealed behind walls. Final and 11-month warranty inspections protect you through the first year.

What are MUD and PID taxes?

Special taxing districts that fund infrastructure and amenities in new communities. They can add $200 to $400 per month. MUD rates typically decline over time. PID terms run 20–40 years. Always ask for the total effective tax rate before committing.

The Bottom Line: Buy with Your Eyes Open

New construction in DFW offers real advantages: modern floor plans, energy efficiency, lower immediate maintenance, builder incentives that can materially reduce your cost of entry, and — in a resale market constrained by the lock-in effect — significantly more available inventory.

On the other side, resale buyers should budget for the deferred maintenance reality. In DFW, homes built before 2010 commonly need fifteen to twenty-five thousand dollars in HVAC replacement, roof repair, or foundation work within the first few years of ownership. Neither path is maintenance-free — the question is whether you prefer known new-build costs or unknown resale surprises.

But the advantages only materialize when the purchase is driven by analysis rather than marketing. The buyers who win in new construction are the ones who underwrite the real monthly payment, negotiate incentives based on their specific financial position, and treat the transaction with the same rigor they would apply to any major investment.

That is the approach we bring to every client at Paragon Realty Advisors. We are not anti-new construction or pro-resale. We are pro-math. And the math always tells the truth.

Ready to evaluate new construction in DFW with a data-driven approach? Let’s connect and build your decision framework together.

Phone: (469) 290-7593

Visit: paragondfw.com/contact

Related Articles

The Buyer’s Blueprint: A Strategic Guide to Dallas Real Estate — paragondfw.com/blog/the-buyers-blueprint-a-strategic-guide-to-dallas-real-estate

Understanding Closing Costs in Texas — paragondfw.com/blog/understanding-closing-costs-in-texas-a-comprehensive-guide-for-buyers-and-sellers

The Texas Third Party Financing Addendum — paragondfw.com/blog/the-texas-third-party-financing-addendum-a-buyers-ultimate-safety-net

Navigating Texas Real Estate Contracts — paragondfw.com/blog/navigating-texas-real-estate-contracts-a-masterclass-on-contingencies-and-addenda