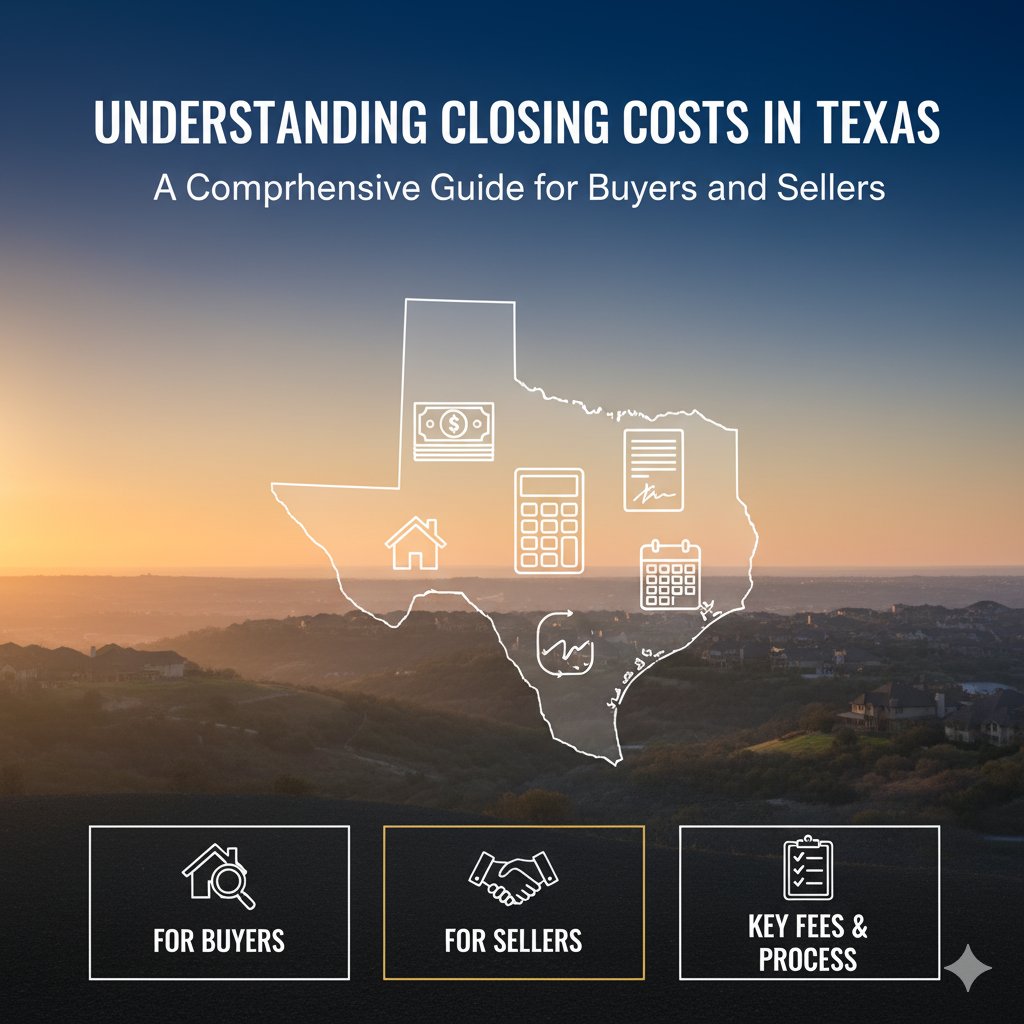

Key Takeaways

• Buyer closing costs in Texas typically range from 2% to 6% of the home's purchase price, while seller costs are higher at 6% to 10%, largely due to the real estate agent commission.

• While customs exist for who pays which fee, nearly all closing costs are negotiable, and the legally binding sales contract is the final authority on the division of expenses.

• Texas has unique financial rules that impact closing, including the significant benefit of no state transfer tax, state-regulated title insurance rates that cannot be shopped for on price, and a "paid in arrears" property tax system that makes proration a critical point of negotiation.

• The seller concession is a key negotiating tool where the seller agrees to pay a portion of the buyer's closing costs, but it is limited by the property's appraised value and the buyer's loan type.

Understanding Closing Costs in Texas: A Comprehensive Guide for Buyers and Sellers

The finalization of a Texas real estate transaction, known as the closing, involves a series of third-party expenses called closing costs. These are separate from the property's purchase price and the buyer's down payment, representing fees for services required to transfer ownership and secure a mortgage. For effective financial planning, buyers and sellers can use general benchmarks. A homebuyer in Texas should anticipate closing costs ranging from 2% to 6% of the home's purchase price. Based on the 2024 median Texas home price of $354,300, this translates to an estimated $7,086 to $21,258. A seller's costs are typically higher, falling between 6% and 10% of the sale price. However, this range is overwhelmingly influenced by a single item: the real estate agent commission, which averages 5.64% to 6% in Texas. When this substantial expense is isolated, the seller's remaining transactional fees average a much more modest 3.48%. While long-standing customs often suggest who pays for which fee, the legally binding sales contract is the ultimate authority, and many costs are explicitly negotiable.

A significant financial benefit for those involved in Texas real estate is the absence of any state or local real estate transfer tax. These taxes, common in many other states, can add thousands of dollars to transaction costs. The lack of a transfer tax in Texas contributes to a more moderate closing cost environment, making the state a more favorable market for both buying and selling property.

In Texas real estate, the division of financial responsibilities between the buyer and seller has historically been governed by established conventions. These customs have created a predictable framework, with two of the most significant being the seller's payment of the commission for both agents and the seller's responsibility to purchase the owner's title insurance policy for the buyer. However, these conventions are not static. Market conditions are leading to an evolution in these customs, and long-assumed responsibilities are increasingly becoming points of negotiation.

The buyer's portion of closing costs is primarily associated with securing a mortgage and performing due diligence. These expenses fall into several key categories. Mortgage-related fees include the loan origination fee, typically 0.5% to 1% of the loan amount, which translates to $1,500 to $3,000 on a $300,000 loan. Property-related fees cover services that assess the home's value and condition, such as the lender-required appraisal, which in a major market like Dallas-Fort Worth typically ranges from $500 to $750. Title and insurance fees include the mandatory lender's title insurance policy and a share of the title search fee. Finally, buyers must fund an escrow account with prepaid items, including the first full year's homeowner's insurance premium, prorated property taxes, and potentially Private Mortgage Insurance (PMI) if their down payment is less than 20%.

The seller's closing costs, which generally range from 6% to 10% of the sale price, are deducted from their proceeds. The single largest expense is the real estate agent commission, which the seller customarily pays for both their agent and the buyer's agent. Sellers may also incur attorney fees if they hire legal counsel. Another significant cost is the owner's title insurance policy, which the seller traditionally purchases to protect the buyer against future title defects. To transfer a clear title, sellers must also pay off their existing mortgage, cover prorated property taxes and HOA dues for their period of ownership, and pay for any required HOA documents. Lastly, sellers are responsible for government recording fees to officially clear their mortgage lien from public records.

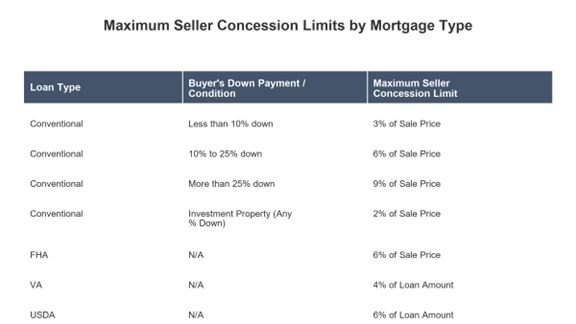

Beyond costs typically assigned to one party, a number of fees are commonly shared or subject to negotiation. Fees charged by the title or escrow company for managing the closing process are often split evenly between the buyer and seller, as are the costs for the title search and any notary services. A powerful negotiating tool is the seller concession, where the seller agrees to pay a portion of the buyer's closing costs. This can make a property more affordable for a buyer, especially in markets with high interest rates. However, there are critical limitations. Concession funds can never be used for the buyer's down payment, and the strategy is constrained by the property appraisal. For instance, a seller might agree to a $306,000 sale price with a $6,000 concession on what is truly a $300,000 home. This strategy fails if the property appraises for less than the inflated $306,000 price, as the buyer's financing could be jeopardized. The maximum amount a seller can contribute is also strictly limited by the buyer's loan type.

The system for title insurance in Texas is unique because it is fully regulated by the Texas Department of Insurance (TDI). The TDI sets the rates, rules, and forms that all title companies must use, meaning the basic premium for a policy is identical regardless of the provider chosen. Consequently, consumers cannot shop for a lower price on title insurance; instead, they should choose a title company based on the quality of its service, responsiveness, and reputation. The premium is calculated using a tiered rate structure based on the property's value, with different rates applied to different value brackets.

Property tax proration in Texas is governed by the state's "paid in arrears" system, where the tax bill for a given year is not due until late in that year or early the next. At closing, the seller must credit the buyer for the property taxes covering the portion of the year the seller owned the home. The buyer then becomes responsible for paying the entire annual tax bill when it comes due. This process can become complicated when the seller has tax exemptions, such as a Homestead or Over-65 exemption, that the buyer does not qualify for. This discrepancy creates a lower tax liability for the seller than what the buyer will eventually face. The financial gravity of this issue is significant: a closing on a property with a $10,000 non-exempt tax bill versus a $4,000 exempt bill could create a proration dispute of over $4,000. This makes the method for calculating the prorated credit a critical point of negotiation that must be clearly defined in the contract.

While many closing costs are standardized, certain fees vary significantly across Texas. Property taxes are the most variable, as they are set at the local level. For example, the average effective property tax rate in Dallas County is 1.73%, but a property within the Dallas Independent School District is subject to a combined local rate of over 2.2%. This directly impacts the prorated taxes due at closing and the size of the required escrow deposit. Additionally, fees for professional services like appraisals and attorney consultations tend to be higher in major metropolitan areas such as Dallas, Houston, and Austin, reflecting a higher cost of living and greater demand.

To navigate the closing process effectively, buyers should adopt several key strategies. It is crucial to shop for a mortgage by obtaining Loan Estimates from at least three different lenders. This creates competition and provides leverage to negotiate lower lender fees. Three days before closing, the buyer will receive a Closing Disclosure, which must be meticulously compared to the initial Loan Estimate to identify and question any new or increased charges. Buyers must also budget comprehensively, accounting not only for the down payment and direct closing costs but also for the initial deposit needed to fund the escrow account. Finally, buyers should investigate state programs like "My First Texas Home," which can provide valuable assistance with closing costs and down payments.

Sellers can also take strategic steps to protect their financial interests. Early in the process, a seller should request a detailed Seller's Net Sheet from their agent to get a realistic estimate of their final proceeds after all costs are deducted. While custom dictates that sellers pay for the owner's title policy, they should view this as a negotiable item, especially in a competitive market. If the seller benefits from tax exemptions, the method for prorating taxes should be proactively addressed during contract negotiations to prevent disputes. If offering a seller concession, the seller must price the home strategically to ensure the contract price will be supported by the appraisal, mitigating the risk of the deal falling through.

The process of closing a real estate deal in Texas involves significant financial commitments and a complex web of customs and legal duties. However, it is a manageable process. The power of proactive diligence cannot be overstated. By thoroughly understanding the purpose of each fee, the customary division of costs, and the key points of negotiation—backed by a clear grasp of the real-world financial stakes—both buyers and sellers can navigate the transaction with confidence, avoid costly surprises, and achieve a financially sound and successful outcome.