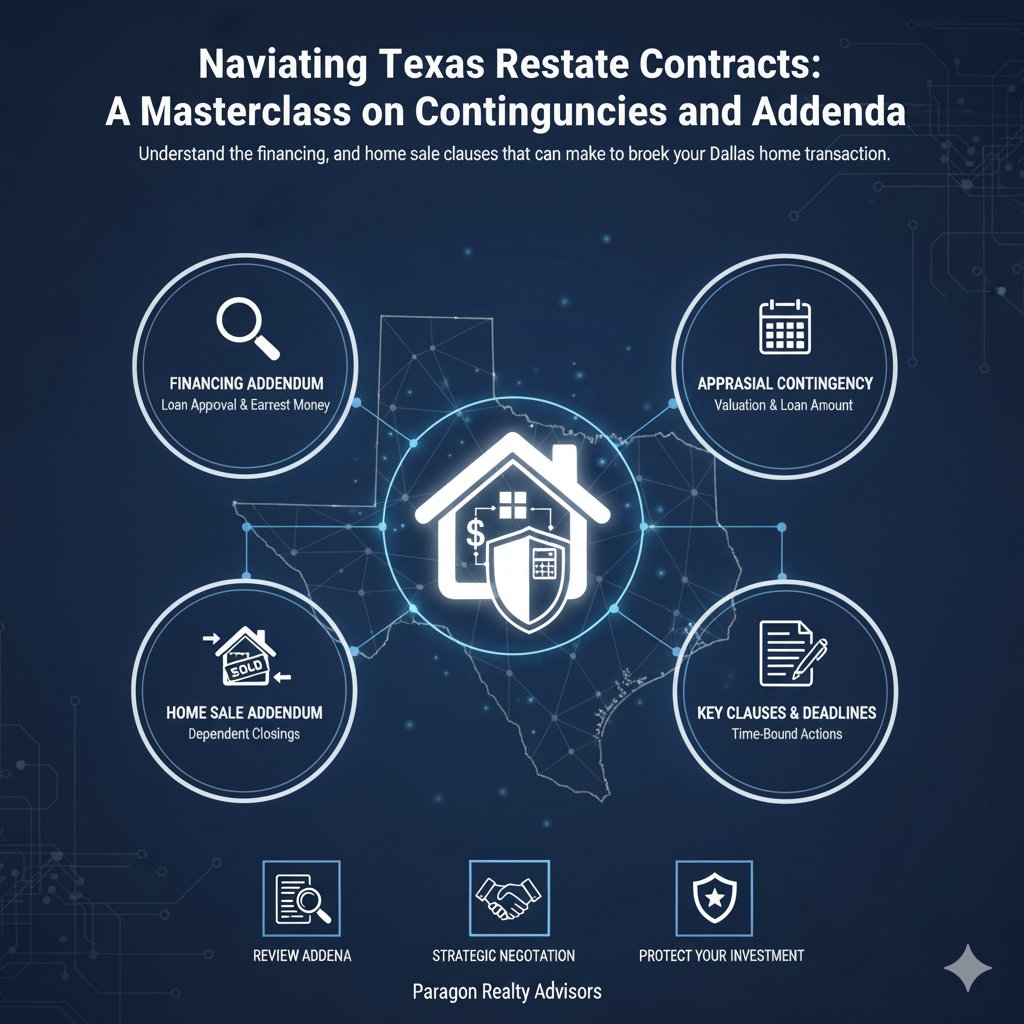

Key Takeaways

• The critical negotiations in a Texas real estate deal occur in the contingency addenda, not the standardized purchase contract; these addenda function as "escape clauses" that allocate financial risk between the buyer and seller.

• The most important contingencies for a buyer are for financing and appraisal. In a competitive market, buyers can make their offers stronger by shortening the financing approval period and by using an addendum to waive or partially cover a potential appraisal gap.

• The Home Sale Contingency, which makes a deal dependent on the buyer selling their current property, creates significant uncertainty for a seller, who can mitigate this risk by negotiating a "kick-out clause" with a short response time.

Buying or selling a home in the dynamic Dallas real estate market is a significant financial undertaking. While negotiations over price and location capture the most attention, the true high-stakes game is played within the legal framework of the purchase contract. This is a masterclass on the Texas real estate contract, its critical addenda, and the art of negotiating the contingencies that can make or break a deal.

The Foundation of Your Texas Home Purchase

Before delving into specific clauses, it is essential to understand the foundational documents that form the bedrock of every residential resale transaction in Texas. The state's use of standardized forms creates a predictable landscape, but mastery of the modular components is what separates a protected party from a vulnerable one.

At its core, a real estate contingency is a provision within a purchase contract that must be met for the agreement to become legally binding. These clauses function as critical "escape clauses" that protect a buyer's earnest money deposit if specific conditions are not satisfied. They are powerful, actively negotiated tools that allocate risk between the buyer and the seller. It is also vital to distinguish between two related legal terms.

• Addendum: A document that adds new terms or conditions to a contract *before* it is signed and executed by all parties.

• Amendment: A document used to modify the terms of a contract that has *already* been executed.

The central document in nearly every single-family home sale in Texas is the One to Four Family Residential Contract (Resale), designated as TREC Form 20-18. Its use by licensed agents is mandatory, creating a predictable framework. This uniformity, however, can create a false sense of security. The contract serves as a foundational "chassis," but the contingency addenda function as the "engine" that drives the deal's specific terms and risk profile. The form itself outlines the fundamental components of the agreement in key paragraphs:

• Paragraph 1: Parties: Identifies the legal names of the buyer and seller.

• Paragraph 2: Property: Provides the legal description of the property.

• Paragraph 3: Sales Price: States the total sales price.

• Paragraph 5: Earnest Money: Specifies the earnest money deposit details.

• Paragraph 6: Title Policy and Survey: Outlines who pays for the title policy.

The standard TREC contract is rarely used in isolation; specific addenda address the unique circumstances of each transaction. The legal and strategic battleground effectively shifts to these modular documents. The most frequently used addenda in the Dallas market include the Third Party Financing Addendum, the Addendum Concerning Right to Terminate Due to Lender's Appraisal, and the Addendum for Sale of Other Property by Buyer. Other common forms address mandatory HOA memberships, lead-based paint disclosures for homes built before 1978, the inclusion of personal property (Non-Realty Items Addendum), and situations where the seller needs to remain in the property after closing (Seller's Temporary Residential Lease).

The Financing Contingency: Your Financial Safety Net

For most buyers, the financing contingency is the most crucial protection. It is formalized through the Third Party Financing Addendum (Form 40-11), which makes the contract contingent on the buyer's ability to successfully secure a loan. If the buyer acts in good faith but is ultimately unable to obtain financing approval, they can terminate the contract and have their earnest money refunded.

The addendum clarifies that loan approval is a dual-hurdle process, creating two distinct periods of risk.

The first pillar, Buyer Approval (Paragraph 2A), concerns the lender's comprehensive evaluation of the buyer's financial standing, including their credit, income, and assets. This approval is tied to a negotiated deadline, and the length of this period becomes a key point of leverage. A buyer with strong finances can confidently agree to a shorter period (e.g., 14-17 days), making their offer more attractive than a competing one with a riskier financing period of 21 days or more.

The second pillar is Property Approval (Paragraph 2B), where the lender underwrites the collateral itself. This includes the appraisal, the property's insurability, and any lender-required repairs. A deal can fail at this later stage if the property is deemed uninsurable or requires significant repairs, meaning the risk for the seller extends well beyond the Buyer Approval deadline.

The Appraisal Contingency: Protecting Your Value Proposition

While the appraisal is just one component of Property Approval, it is often the most contentious. This contingency protects the buyer from being obligated to purchase a property for more than its lender-verified fair market value. When a licensed appraiser determines the home's value is less than the agreed-upon sales price, it creates a financing "gap" that must be bridged. For example, on a $500,000 sales price with a 20% down payment, the buyer is seeking a $400,000 loan. If the property appraises for only $480,000, the lender will only finance 80% of that appraised value, or $384,000. This leaves a $16,000 gap that the buyer must cover for the deal to close.

In this situation, a buyer has three primary options: renegotiate the sales price with the seller, terminate the contract and recover their earnest money, or cover the appraisal gap with their own cash. For competitive markets like Dallas, TREC provides an advanced tool: the Addendum Concerning Right to Terminate Due to Lender's Appraisal. This form allows a buyer to modify or waive their termination rights. It presents three choices: a full waiver, which is the strongest signal to a seller but carries the most risk for the buyer; a partial waiver that sets an "appraisal floor," capping the buyer's cash exposure to a specific amount; or an additional right to terminate based purely on value, independent of financing.

The Home Sale Contingency: Navigating the Domino Effect

The contingency that makes a seller's property most vulnerable is the one that ties the transaction to the success of an entirely separate deal. The Addendum for Sale of Other Property by Buyer (Form 10-6) is used when a buyer's purchase is financially dependent on selling their existing home. For the buyer, this provides ultimate protection against the burden of owning two homes simultaneously. For the seller, it introduces massive uncertainty.

To counteract this risk, the addendum contains a powerful mechanism known as a "kick-out clause." This provision allows the seller to continue marketing their property. If the seller receives another acceptable offer, it triggers a "fish or cut bait" moment for the first buyer. The seller provides written notice, and the first buyer then has a short, pre-negotiated period (typically 24 to 72 hours) to either waive the home sale contingency and commit to the purchase, or terminate the contract and have their earnest money returned. The negotiation over the length of this response time is a critical point of leverage for the seller.

Expert Recommendations for the Dallas Market

The power to negotiate contingencies is dictated entirely by market conditions. In a strong seller's market like Dallas, sellers hold the leverage and can demand that buyers limit or waive contingencies. In a buyer's market, the power shifts. The following strategies are crucial for navigating these dynamics.

For Buyers

Get Financially Fit First: Secure a full, underwritten pre-approval from a reputable local lender before making an offer. This demonstrates your capacity and allows you to confidently agree to a shorter financing period.

Prepare for Appraisal Gaps: Analyze your finances to determine the maximum cash you can bring to closing to cover a potential gap. Use the partial waiver option in the appraisal addendum strategically to communicate this commitment while capping your risk.

Avoid the Home Sale Contingency if Possible: This contingency makes an offer exceptionally weak in a seller's market. Explore alternatives like a bridge loan or selling your current home first.

For Sellers

Scrutinize the Financing Terms: Look beyond the offer price. Favor offers with shorter financing periods, larger down payments, and buyers using well-known local lenders.

Negotiate Contingencies Aggressively: In a strong market, push for full or partial appraisal waivers. If you accept a home sale contingency, insist on a very short response time for the kick-out clause (e.g., 24-48 hours) to minimize your property's time in limbo.

Always Rely on Professional Counsel: A skilled real estate agent and attorney are essential partners for navigating complex negotiations from a position of strength and knowledge.

The standardized Texas real estate contract and its associated addenda constitute the rulebook for a high-stakes financial transaction. A comprehensive understanding of how these contingencies function individually and as an interconnected system is paramount. This knowledge empowers buyers and sellers to move beyond simply signing forms, allowing them to negotiate intelligently, mitigate risk, and ultimately close their transactions with confidence.