Key Takeaways

• The Third Party Financing Addendum is a contractual safety net that allows a home buyer to terminate the purchase and get their earnest money back if their loan is denied for specific financing-related reasons.

• The buyer has an active, time-sensitive duty to provide written notice of termination by a strict deadline; failing to do so waives this protection and puts their earnest money at risk.

• A 2025 update will require buyers terminating for a lack of "Buyer Approval" to provide a written statement from their lender detailing the specific reason for the loan denial.

• The form contains two distinct contingencies: "Buyer Approval," which concerns the buyer's personal financial situation, and "Property Approval," which concerns the lender's acceptance of the property itself (including its appraisal and condition).

If you’re buying a home in Texas with a loan from a bank or mortgage company, you will encounter the Third Party Financing Addendum. This standard form is your most important safety net. In simple terms, it is your contractual "escape hatch"—a legal pathway that allows you to back out of a purchase contract and get your earnest money deposit back if your loan doesn't get approved for specific, financing-related reasons. This protection is crucial, as it prevents you from forfeiting your earnest money due to unexpected lending issues that are often beyond your control.

To ensure consistency and fairness, the Texas Real Estate Commission (TREC) mandates the use of this form. This standardization brings order to a process that could otherwise be chaotic, but its true value lies in the clarity it has evolved to provide.

The Evolution from Ambiguity to a Bright-Line Test

The addendum has undergone a significant evolution. Early iterations of the form were centered on an ambiguous concept of "Credit Approval," which created considerable uncertainty for both buyers and sellers. It was often unclear when, or if, a lender’s conditional approval satisfied the contract, leading to frequent disputes.

To resolve this, TREC fundamentally shifted the form's legal philosophy. The modern addendum moved away from a passive condition (waiting for "approval") to an active, procedural duty placed upon the buyer. The responsibility is now on you, the buyer, to provide timely, written notice of termination if you cannot obtain financial approval within a specified number of days. If you fail to act before the deadline, your protection is waived. This shift replaced a subjective debate over the definition of "approval" with an objective, bright-line test: was the termination notice delivered on time? This provides critical certainty for both parties.

The 2025 Update: Hardening the Buyer Approval Contingency

Starting January 3, 2025, a significant change to the form takes effect, designed to increase transparency and fairness. The update hardens the termination right for Buyer Approval in Paragraph 2A.

Previously, a buyer could terminate due to a lack of Buyer Approval with a simple notice. Under the new rule, you will be required to provide not just a notice of termination, but also a written statement from your lender that details the specific reason for the loan denial. This change creates "procedural parity" with the long-standing evidentiary requirement for a Property Approval termination. It ensures the seller receives verifiable proof that the termination is legitimate and prevents the financing contingency from being misused as a loophole for "buyer's remorse."

A Forensic Walkthrough of the Form

Understanding the form requires a line-by-line analysis. The header simply requires the property's street address and city, which must match the main purchase contract exactly.

Paragraph 1: Type of Financing and Duty to Apply

This section details the specific loan you are trying to obtain and establishes your legal obligation to "apply promptly" and "make every reasonable effort" to get it approved. This means you must act in good faith; you cannot simply fail to submit your documents to the lender and then use this form to terminate.

You and your agent will check the box that corresponds to your loan type (e.g., Conventional, FHA, VA). For most loan types, you must specify the loan amount, the term (length of repayment), and a cap on origination charges. You will also fill in a "not to exceed" interest rate. This is a key protection that prevents you from being forced to accept a loan if rates spike. Agents often set this ceiling higher than the current market rate to give you more flexibility. However, an unreasonably high rate might be viewed by a seller as a red flag, signaling that you are creating an easy exit from the contract, which could make your offer less attractive.

Paragraph 2: Approval of Financing

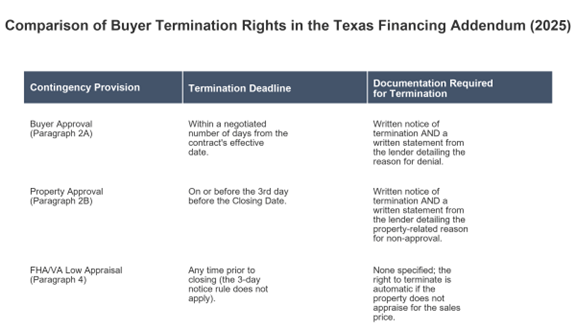

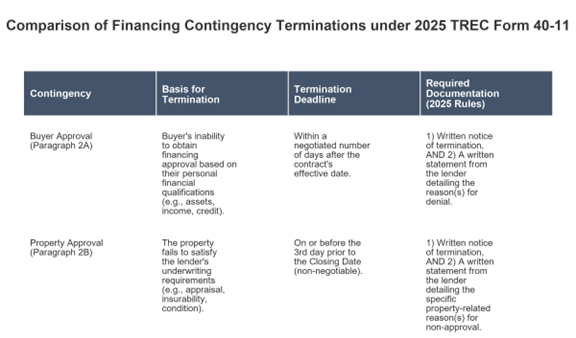

This is the functional core of the addendum, where your right to terminate—your contingency—is defined. It begins with the legal phrase "Time is of the essence," a stern warning that all deadlines in this section are firm and must be followed perfectly. The paragraph is split into two distinct contingencies: Buyer Approval and Property Approval.

A. Buyer Approval: This contingency is based on the lender's approval of *you*, the borrower. The lender performs a deep dive into your personal financial situation, including your income, assets, and credit history.

You and your agent will fill in what is arguably the most critical blank on the form: the number of days you have to either secure this approval or terminate. It is one of the most frequent and dangerous misconceptions to let this deadline pass with only a simple "pre-approval" letter. True "Buyer Approval" only occurs after your loan file has been forensically examined by the lender's underwriter, a process that can take weeks. If this deadline expires and the underwriter later denies the loan, your earnest money is at risk.

To terminate under this paragraph, the 2025 rules require you to give the seller written notice of termination *and* a written statement from your lender explaining why you were denied, all before the deadline expires. You can also check a box to waive this right entirely. This makes your offer much stronger to a seller, but it is extremely risky and should only be considered if you are absolutely certain your loan will be approved.

B. Property Approval: This contingency is based on the lender's approval of the *property* itself. The lender must be satisfied that the house is a sound investment, which includes its appraisal value, condition, and insurability. The deadline for this contingency is fixed: you have until three days before the closing date to terminate for a property-related financing issue. To do so, you must provide the seller with written notice and a written statement from the lender that explains the specific reason the property failed to meet their underwriting requirements (e.g., an insufficient appraisal or the home being uninsurable).

Paragraph 3: Security

This is standard legal language that states the loan will be secured by the property itself. It establishes the lender's legal right to foreclose if you fail to make your payments as agreed.

Paragraph 4: FHA/VA Required Provision

If you are using an FHA or VA loan, this paragraph provides a powerful, extra layer of protection. It acts as an appraisal "super-contingency," stating that if the property does not appraise for at least the sales price, you are not obligated to complete the purchase and can have your earnest money refunded. Critically, this right extends all the way to the closing date and is not subject to the three-day deadline in Paragraph 2B. If the appraisal is low, you still have the option to proceed by paying the difference in cash, or the seller may agree to lower the sales price.

Paragraph 5: Authorization to Release Information

This practical clause gives your lender and the title company permission to share information about your loan status with your agent and the seller's agent. This ensures all parties are kept informed and helps prevent last-minute surprises before closing.

Frequently Asked Questions

Is this form required?

Yes, if you are obtaining a loan from a third-party lender to buy a home in Texas, your agent is required by law to use this standardized form as part of your offer.

What if I need more time for Buyer Approval?

If your deadline is approaching and your loan is not yet finalized, your agent must act immediately to request an extension from the seller using an "Amendment to Contract" form. The seller can either agree or refuse. If they refuse, you face a difficult choice: terminate before the deadline expires to protect your earnest money, or allow the deadline to pass and risk losing that money if the loan is ultimately denied.

Does this form protect me from a low appraisal?

It depends on the loan type.

• For FHA and VA loans, Paragraph 4 provides an automatic and clear right to terminate if the appraisal comes in below the sales price.

• For a conventional loan, the situation is more nuanced. A low appraisal only allows termination under Paragraph 2B if the lender provides a written statement that the low value specifically causes the property to no longer meet its underwriting requirements. For more direct protection with a conventional loan, your agent should use the separate Addendum Concerning Right to Terminate Due to Lender's Appraisal.

What if the seller won't release my earnest money after I terminate correctly?

If you terminate correctly by providing proper notice and documentation before the deadline, you are contractually entitled to your earnest money. If the seller refuses to sign the release, the title company cannot release the funds without mutual agreement or a court order. Your agent will guide you through the next steps, which may involve demanding mediation as specified in the contract or pursuing legal action.