Key Takeaways

• The Texas homestead exemption has two distinct and separate functions: a powerful, constitutionally-guaranteed shield protecting a primary residence from most creditors and a separate, legislatively-controlled system for providing significant property tax relief.

• The creditor protection is one of the strongest in the nation, offering unlimited monetary protection against the forced sale of a home to satisfy general debts, with only eight specific, constitutionally-enumerated exceptions.

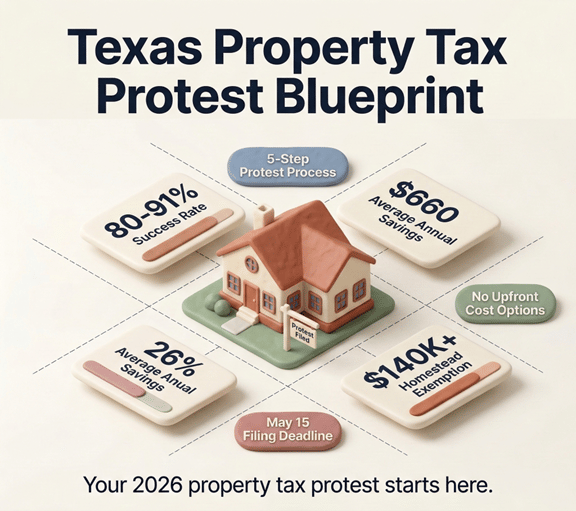

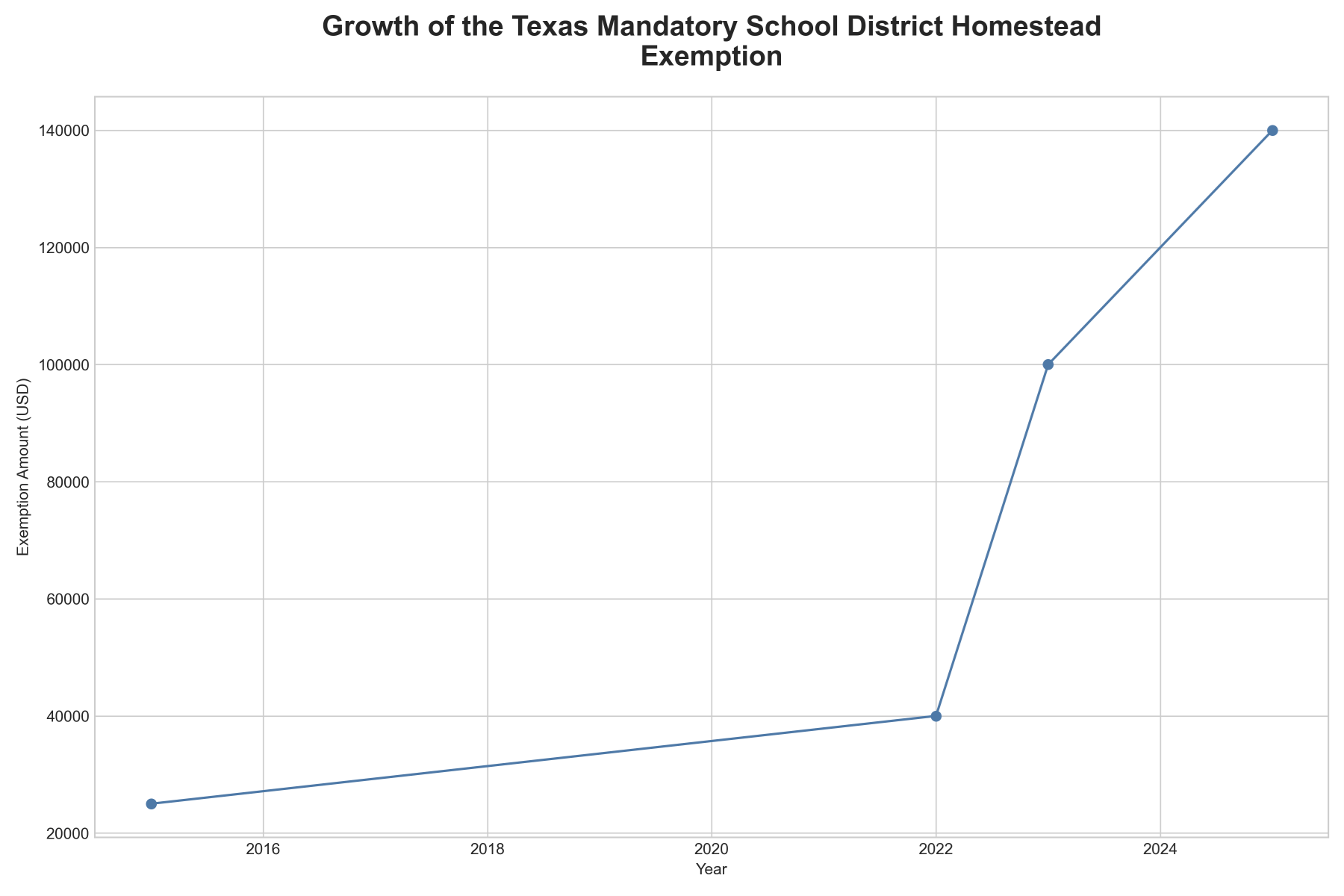

• The property tax relief component, primarily through a large mandatory school district exemption ($100,000 in 2023) and a 10% cap on annual appraisal increases, has major economic consequences, shifting the tax burden from homeowners to renters and businesses and creating housing market distortions.

The Two Sides of the Texas Homestead Exemption: Creditor Shield and Tax Relief

The Texas homestead exemption has a dual identity, functioning as both a powerful constitutional shield protecting homeowners from creditors and a significant mechanism for property tax relief. The creditor protection, rooted in Article 16, Section 50 of the Texas Constitution, is the law's original and most stable feature. It provides an almost absolute defense against the forced sale of a primary residence to satisfy general debts, offering unlimited monetary value with only eight specific exceptions. In contrast, the ad valorem tax exemption, authorized by Article 8, Section 1-b, is a more recent and politically dynamic tool of state fiscal policy. It reduces the taxable value of a home, with the mandatory school district exemption seeing exponential growth to $100,000 in 2023. A key feature enhancing this relief is the homestead cap, which limits the annual increase in a property's appraised value for tax purposes to 10 percent, providing predictability for homeowners but also creating market distortions. These policies have profound economic consequences, necessitating a massive fiscal transfer from the state's general revenue to reimburse local school districts. This effectively shifts the tax burden from homeowners to a broader base of consumers, renters, and businesses, reshaping the state's economic landscape.

The origins of the Texas homestead law are found not in tax policy but in the necessity of frontier settlement, where attracting immigrants and protecting them from past financial troubles was essential for the growth of the new republic. The law's primary purpose was robust creditor avoidance. Tracing its lineage to Spanish and Mexican colonization laws of the 1820s, Texas established itself as a sanctuary for debtors by passing a law in 1829 that shielded colonists' lands from seizure for debts contracted before their arrival. This debtor-centric philosophy was formally codified in the landmark Texas Act of 1839, the first law of its kind to establish a homestead exemption, protecting a family's home from economic disaster. This principle was so fundamental that it was elevated into successive state constitutions, securing it from easy legislative change. Over time, the law's purpose has evolved from its 19th-century agrarian ideal. A key 1973 amendment extended protections to single adults, and today the law serves a dual role as both an unwavering creditor shield and a highly flexible instrument for property tax relief.

The Texas homestead right is comprised of two distinct legal pillars, each founded on a separate article of the state constitution. The first and most formidable is the protection from forced sale, which operates as a direct and potent shield for homeowners. Based in Article 16, Section 50, this provision establishes a general rule of immunity for a primary residence, extending to the full value of the qualifying property. Any lien against a homestead that does not fall into one of eight specific, constitutionally enumerated exceptions is considered void. The eight exceptions are:

• Purchase Money: A loan used to acquire the property itself.

• Taxes Due Thereon: Ad valorem property taxes owed on the homestead.

• Owelty of Partition: A lien used to equalize the division of property between co-owners, typically in a divorce.

• Refinance of a Valid Lien: A new loan taken out to pay off an existing, valid lien against the homestead.

• Work and Material for Improvements: A lien for the cost of construction or repairs, which requires a specific written contract with consumer protections.

• Extension of Credit (Home Equity Loan): A loan allowing homeowners to borrow against their equity. These loans are subject to a detailed set of regulations embedded directly into the Texas Constitution, transforming it into a "quasi-regulatory code." This unique feature makes the consumer protections—such as an 80% loan-to-value cap, non-recourse provisions, and a 12-day cooling-off period—exceptionally stable and reflects a deep, historical distrust of lenders.

• Reverse Mortgage: A loan for homeowners aged 62 or older that converts home equity into cash, subject to its own constitutional rules.

• Converted Manufactured Home Lien: A valid lien on a manufactured home established before it was attached to the land.

The Texas Property Code defines the physical extent of the homestead, allowing for up to 10 acres for an urban homestead and up to 200 acres for a family's rural homestead. A critical ancillary protection is the six-month proceeds rule, which exempts the cash from the sale of a homestead from creditors for six months, allowing the homeowner time to reinvest in a new homestead. The second pillar is relief from ad valorem property taxes, based on the permissive language of Article 8, Section 1-b, which authorizes the Legislature to create tax exemptions. Implemented through the Texas Tax Code, this benefit is a creature of legislative policy rather than a fixed constitutional right. This creates a fundamental legal distinction: the creditor shield is an absolute right for asset preservation, while the tax exemption is a legislatively controlled reduction in the annual cost of homeownership. For example, a homeowner with a 150-acre rural property could be fully protected from creditors under Article 16, but would only receive the tax exemption on the residence and 20 of those acres under Article 8, clarifying the context-dependent nature of the "homestead."

The Texas system of property tax exemptions is a layered structure of state-mandated benefits and local options. The cornerstone of relief is the mandatory school district exemption, which is available to every qualified homeowner. This exemption has grown dramatically, increasing from $25,000 to $40,000 in 2022 and then to $100,000 for the 2023 tax year. Texas also provides targeted relief for vulnerable populations. Homeowners who are 65 or older or are disabled are entitled to an additional $10,000 exemption from school taxes. More importantly, they benefit from a school tax ceiling, which freezes the amount of school taxes they pay in the year they qualify, protecting them from future increases in property values or tax rates. A separate, generous schedule of exemptions honors disabled veterans. These are tiered based on disability rating, culminating in a 100% total property tax exemption for veterans with a 100% service-connected disability rating. A 100% exemption is also available to the surviving spouses of service members and first responders killed in the line of duty. Beyond these state mandates, local taxing units like cities and counties can offer optional exemptions, most commonly a percentage exemption of up to 20% of the property's value. Finally, recent reforms have addressed challenges for "heir property," now allowing an heir who occupies an inherited home as their principal residence to receive 100% of the available exemptions, even if they only have fractional ownership.

The homestead exemption directly erodes the tax base for local governments. To prevent the defunding of public education, the state has a "hold harmless" provision that uses general revenue to reimburse school districts for the revenue lost due to state-mandated exemption increases. For the 2023 increase, the legislature allocated $5.6 billion for this purpose. This policy effectively shifts the source of school funding from local property wealth to statewide consumer and business activity. Cities and counties that offer optional exemptions receive no such reimbursement, forcing them to either reduce services or increase their property tax rates to compensate. Data reveals how this has played out over 25 years: from 1998 to 2023, while school district levies grew 187%, city and county levies grew far faster, at 257% and 256% respectively, proving how local governments are forced to compensate. An unavoidable consequence of removing residential value from the tax rolls is a shift of the tax burden to commercial, industrial, and residential rental properties. This indirectly affects the 37% of Texas households that are renters, as landlords often pass their higher tax burden on to tenants through increased rents. The exemption also creates significant housing market distortions. While it improves affordability for existing homeowners, the homestead cap creates a powerful "lock-in effect." The substantial tax benefit discourages long-term homeowners from moving, which can reduce the supply of existing homes for sale and create significant tax inequities between neighbors in identical houses.

To receive a homestead tax exemption, a homeowner must file an application with the Central Appraisal District (CAD) in their county, typically between January 1 and April 30. A generous provision allows for late filing up to two years after the delinquency date. The key documentation requirement is a valid Texas Driver's License or ID card with an address that matches the property address. A recent change in law under Senate Bill 1801 now requires CADs to verify each homeowner's eligibility at least once every five years. This new compliance burden means homeowners may receive notices requiring them to re-verify their status. Failure to respond could result in the loss of the exemption, leading to a sudden, substantial increase in their tax bill or a significant mortgage escrow shortage.

Beyond the exemptions, the homestead cap provides another layer of powerful tax protection by limiting annual increases in a home's appraised value. The law dictates that the appraised value of a qualified homestead cannot increase by more than 10 percent from one year to the next. This protection does not begin immediately; it takes effect in the second full calendar year of qualification, with the first year establishing the "base year" value. It is crucial to understand the distinction between the capped appraised value, which is used to calculate taxes, and the market value, which is what the home could sell for. In a rising market, this creates a growing gap between the two figures. The cap is personal to the homeowner and resets upon sale. A new owner's appraisal will be based on the full market value, at which point a new base year is established for them.

The homestead exemption has become the central battleground of modern Texas fiscal policy. The 2023 legislative session delivered an $18 billion property tax cut package, the centerpiece of which was the dramatic increase of the mandatory school district exemption to $100,000. This measure passed with overwhelming bipartisan support and was approved by 83% of voters. The political momentum has continued, with 2025 legislative proposals seeking to further increase the general exemption to $140,000 and the exemption for seniors and disabled persons to an even higher level.

This legislative drive has highlighted a core policy debate. One approach, favored by the Senate, is to increase the fixed-dollar homestead exemption, which provides proportionally greater relief to owners of lower- and middle-value homes. The other approach, generally favored by the House, is tax rate compression, which uses state funds to lower tax rates for all property classes, including businesses and rental properties. The 2023 compromise included both, but the massive exemption increase was the headline achievement.

Nationally, Texas's homestead laws, particularly regarding creditor protection, are among the most generous in the United States. While many states place a cap on the dollar amount of home equity protected from creditors, Texas provides an unlimited shield. This stands in stark contrast to states like California and New York, which offer substantial but ultimately finite protection, making Texas a uniquely attractive state for asset protection.

The Texas homestead exemption has evolved from a simple debtor shield into a complex institution at the nexus of state fiscal policy, local finance, and the housing market. The future appears set on a continued expansion of the tax relief component, a politically popular strategy for returning state budget surpluses to taxpayers. However, this path presents long-term challenges. Each increase narrows the local property tax base, increases the dependence of school districts on state funding, and shifts a greater share of the tax burden onto businesses and renters. The unresolved tension between providing ever-greater tax relief to homeowners and maintaining a broad, stable, and equitable tax base to fund the needs of a rapidly growing state will be the defining challenge for the future of this uniquely Texan institution.