Key Takeaways

• Engage a real estate agent under a formal Buyer Representation Agreement to ensure they are your legal fiduciary, obligated to prioritize your interests above all others.

• Secure a mortgage pre-approval before beginning your home search to establish a strong financial foundation and make your offer more competitive in the Dallas market.

• Conduct diligent, Dallas-specific investigations, focusing on potential foundation problems caused by expansive clay soil and carefully evaluating the condition of the roof and HVAC system due to the extreme climate.

• After a home inspection, it is strategically better to negotiate for a seller credit or a price reduction rather than asking the seller to make repairs, as this gives you full control over the quality of the work.

The Buyer's Blueprint: A Strategic Guide to Dallas Real Estate

A successful home purchase in the Dallas market is not a matter of chance but the result of a systematic process. This framework is built upon three essential pillars: securing legally-bound, expert fiduciary representation; establishing a rigorously vetted financial foundation through mortgage pre-approval; and executing diligent, market-specific investigations into a property's legal and physical integrity. This structured approach provides buyers with a distinct competitive advantage while mitigating significant financial risk throughout the transaction.

The Foundation: Your Fiduciary Agent

The Dallas real estate landscape is shaped by foundational elements that every prospective buyer must understand, including non-negotiable legal standards and unique environmental challenges. In Texas, the buyer-agent relationship is governed by a legal mandate of fiduciary duty, codified by the Texas Real Estate Commission (TREC). This legal framework is built upon specific canons of professional ethics that all license holders must follow.

• Fidelity: This paramount duty requires the agent to place the client's interests above all others, including their own, ensuring they act scrupulously and meticulously.

• Integrity: An agent has a special obligation to exercise prudence and caution to avoid misrepresentation, whether by commission or omission.

• Competency: This standard demands an agent be informed about local market conditions, stay educated on industry developments, and exercise sound judgment and skill in their specific geographic area.

Beyond the legal framework, the geological and climactic imperatives of North Texas dictate a buyer's due diligence. The region's expansive clay soil, which swells when wet and shrinks when dry, exerts immense pressure on home foundations, making it a primary cause of structural issues. Furthermore, the extreme climate, characterized by intense summer heat, high humidity, and severe storms, places significant demands on a home's core systems, particularly the roof and HVAC unit.

A buyer's agent is legally bound by fiduciary duties, a concept often summarized by the OLDCAR framework. These duties are not just abstract terms; they are a buyer's strategic advantage in a transaction.

• Obedience: The agent must obey all of the client's lawful instructions.

• Loyalty: The agent must act solely in the client's best interest. This prevents an agent from steering a buyer toward a pricier home simply to earn a higher commission, a direct conflict of interest.

• Disclosure: The agent must disclose all material facts and information that could benefit the buyer's position.

• Confidentiality: The agent must keep the client's personal and financial information confidential. This means an agent cannot legally reveal a buyer’s maximum budget or motivations to the seller, protecting the buyer's negotiating power. This duty survives the transaction.

• Accounting: The agent must account for all funds and documents, such as earnest money deposits, entrusted to them.

• Reasonable Care: The agent is expected to use their professional skills and expertise to the best of their ability on the client's behalf.

These legal protections are formalized through a Buyer Representation Agreement (BRA), a written contract that transforms a buyer from a "customer" to a "client" with full fiduciary rights. Without a BRA, an agent showing a property is legally considered a sub-agent of the seller. A truly exceptional agent operates under a proactive model, going beyond the baseline fiduciary duties to create value. This includes leveraging professional networks to find off-market opportunities, providing deep market analysis to inform decisions, and offering strategic counsel to navigate complex negotiations and multiple-offer situations.

Financial Strategy and Market Snapshot

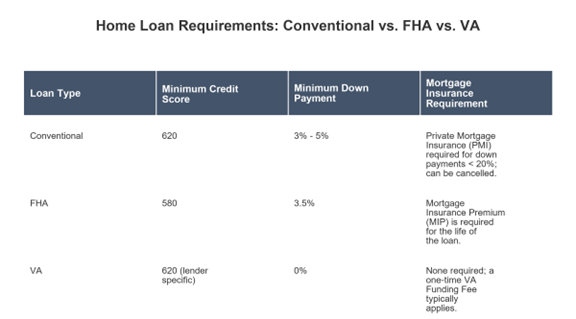

Before the home search begins, a buyer must establish a solid financial strategy, centered on securing a mortgage pre-approval. A pre-qualification is an informal estimate, but a pre-approval is a conditional commitment from a lender based on verified documentation. In competitive markets like Dallas, an underwritten pre-approval, where a loan underwriter has already reviewed all financial documents, provides the strongest position, making an offer nearly as attractive as cash. Lenders evaluate a buyer's profile using the "Four C's": Capital (down payment and reserves), Capacity (debt-to-income ratio), Credit (history and score), and Collateral (the property's value). Buyers in Dallas primarily utilize Conventional, FHA, and VA loans, each with distinct requirements.

Texas also offers a unique state-level financial instrument through the Texas Veterans Land Board (VLB). This program provides competitive, low-interest home loans to eligible veterans and offers an additional interest rate discount for veterans with a service-connected disability rating of 30% or higher.

The current Dallas market can be described as a bifurcated environment. Key performance indicators show an average home value of $311,285, a median time to pending of 33 days, and a median sale-to-list price ratio of 98.4%. While 18.4% of homes sell above list price, indicating bidding wars on desirable properties, 63.2% sell for under list price, suggesting opportunities for negotiation on other homes.

Dallas-Specific Due Diligence

Structural due diligence in Dallas requires a specific focus on local conditions. Foundations are typically either concrete slab-on-grade or pier-and-beam. Buyers should watch for tangible "red flags" indicating potential foundation issues, such as "stair-step" cracks in exterior brickwork, diagonal cracks in interior drywall, and doors or windows that stick or jam.

Roofing systems must be evaluated for their ability to withstand hail, wind, and intense solar heat, with materials like metal and composite offering superior durability. Finally, HVAC systems are a necessity, not a luxury. Buyers should prioritize systems with a high Seasonal Energy Efficiency Ratio (SEER rating of 16 or more) to manage high energy costs. It is critical to be aware that the average lifespan of an HVAC unit is 10-15 years; an older unit represents a significant impending expense.

From Offer to Closing

A competitive offer is built on several components. The offer price should be determined by a data-driven Comparative Market Analysis. Earnest money, typically 1% of the purchase price, is a good-faith deposit held in escrow. The Texas-specific Option Fee is a small, non-refundable payment to the seller that purchases an "option period," usually 7-10 days, during which the buyer can terminate the contract for any reason and have their earnest money refunded. Contractual contingencies provide crucial risk mitigation. The financing contingency allows the buyer to exit the deal if they cannot secure a loan, while the appraisal contingency protects them if the property appraises for less than the contract price.

Two third-party validation processes are critical. The home appraisal, ordered by the lender, provides an independent valuation of the property. If an appraisal comes in low, creating an "appraisal gap," the buyer can renegotiate, cover the difference in cash, or terminate the contract under the contingency. The title company conducts a comprehensive title search to ensure the seller has the legal right to sell and to uncover any liens or claims. An owner's title insurance policy, customarily paid by the seller in Texas, protects the buyer from hidden title defects for as long as they own the property.

The pre-offer phase begins with crafting a clear search strategy based on a "Needs vs. Wants" framework to separate non-negotiable requirements from desirable features. Buyers should leverage technology, starting with public portals for general browsing but relying on their agent's direct MLS client portal for the most accurate, real-time data and agent-only information. To streamline the financing step, a buyer should assemble their mortgage pre-approval document file in advance, including income verification, asset statements, and identification.

During the offer and negotiation phase, a buyer must structure a compelling offer and be prepared for multiple-offer scenarios. This may involve tactics like offering a flexible closing date or a seller leaseback. The Texas Option Period must be used strategically. A buyer should schedule the general home inspection immediately, review the report thoroughly, and if necessary, schedule specialized inspections and obtain repair estimates well before the deadline.

After the inspection, buyers have several negotiation tactics. While requesting the seller to perform repairs is an option, it cedes control over the quality of the work. A more advantageous approach is often to request a seller credit at closing or a reduction in the purchase price. This strategy is superior because it gives the buyer complete control over hiring their preferred contractors and overseeing the repairs to their standards. Furthermore, it is often a simpler, more attractive proposition for a seller who is focused on the logistics of moving rather than managing repairs.

In the closing phase, federal law requires the lender to provide the buyer with the Closing Disclosure (CD) at least three business days before the scheduled closing. This document itemizes all loan terms and costs, and the buyer must conduct a line-by-line review, comparing it to the initial Loan Estimate to ensure there are no surprises. The "Cash to Close" figure on the CD is the final amount the buyer must bring. Just before the appointment, a final walk-through confirms the property's condition has not changed. On closing day, the buyer will sign numerous documents, provide a cashier's check or wire transfer for the closing funds, and receive the keys.

Post-Closing and Long-Term Ownership

Post-closing operations begin immediately. The new homeowner must establish household utilities, including water with Dallas Water Utilities and natural gas with Atmos Energy. For electricity, Texas has a deregulated market, requiring the homeowner to choose a Retail Electric Provider by comparing plans on the state-run PowertoChoose.org website. One of the most critical financial steps is to file for a homestead exemption with the Dallas Central Appraisal District (DCAD) before the May 1st deadline. This exemption significantly reduces the property's taxable value, lowering the annual property tax bill. Finally, implementing a seasonal maintenance plan tailored to the North Texas climate—including foundation watering in the summer and insulating pipes in the winter—is essential for protecting the investment.

Homeownership is an ongoing investment that requires proactive management. The annual property tax cycle involves two key entities: the Dallas Central Appraisal District (DCAD), which appraises property values and approves exemptions, and the Dallas County Tax Office, which bills and collects the taxes. New homeowners should understand their right to protest the appraised value if they believe it is too high. A proactive maintenance regimen is crucial to address the environmental stressors unique to North Texas. By staying on top of these responsibilities and leveraging their agent relationship as a lifelong resource for real estate advice and equity tracking, homeowners can protect and enhance the value of their asset over the long term.

The acquisition of a home in Dallas is a complex, high-stakes financial transaction that demands a methodical and informed approach. Success is contingent not on market timing, but on a buyer's commitment to strategic preparation, the engagement of a true fiduciary advisor, and the execution of rigorous, market-specific due diligence at every stage of the process. This disciplined framework transforms the buyer from a passive participant into a confident, empowered investor, capable of navigating the market's challenges and securing a valuable asset for their future.