Key Takeaways

• A monthly mortgage payment consists of four parts: Principal, Interest, Taxes, and Insurance (PITI). Even on a "fixed-rate" loan, the total payment can change annually due to fluctuations in property taxes and homeowners insurance.

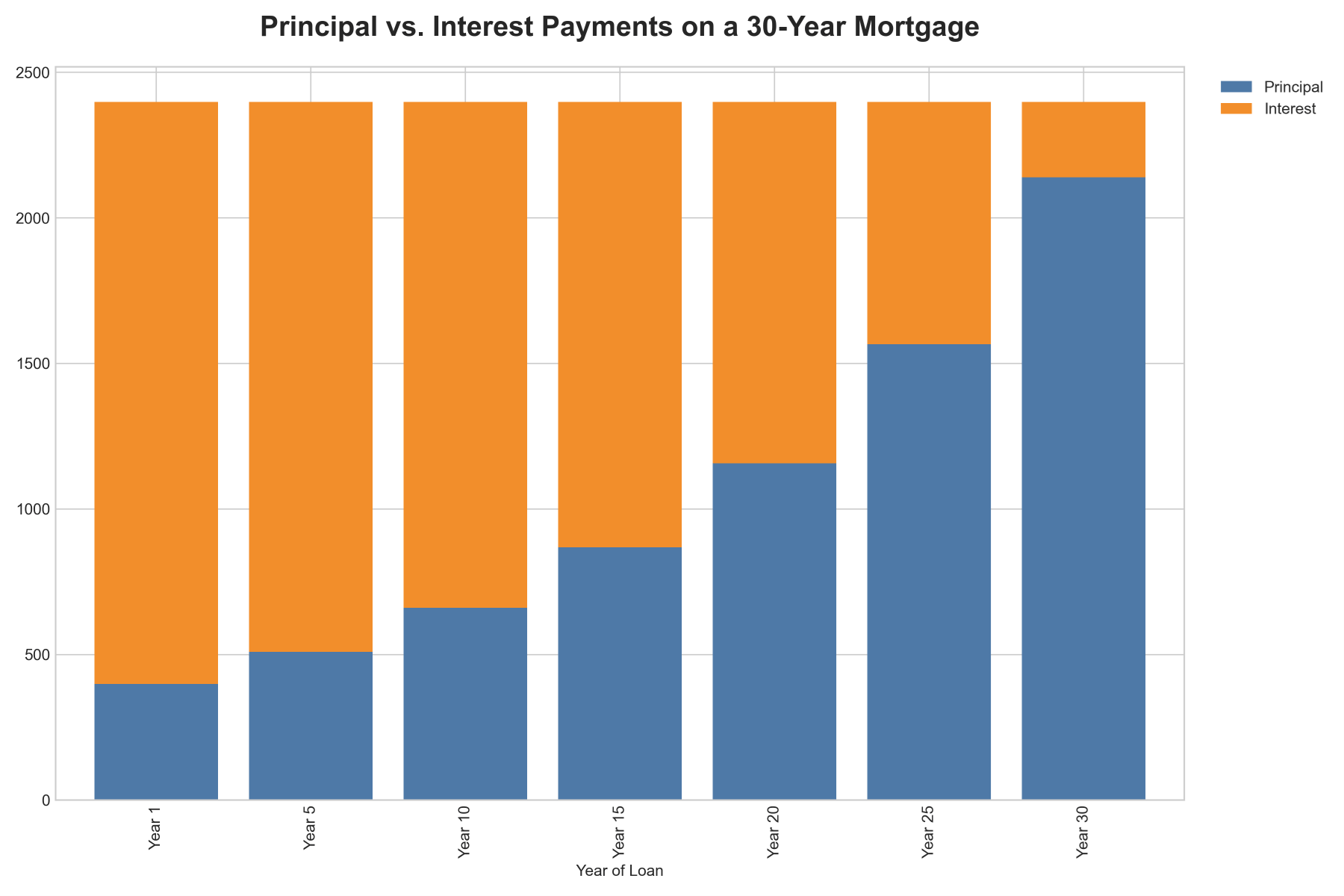

• The interest on a mortgage is front-loaded, meaning the vast majority of payments in the early years of the loan go toward interest rather than reducing the principal balance, causing homeowners to build equity very slowly at first.

• Long-term fixed mortgage rates are not directly set by the Federal Reserve; they are primarily influenced by inflation and the U.S. bond market, with the 10-year U.S. Treasury yield serving as the most direct real-time indicator.

• A small change in the interest rate has a massive impact on both a buyer's purchasing power (a 1% rate increase reduces purchasing power by about 10%) and the total interest paid over the life of the loan.

Deconstructing Your Monthly Mortgage Payment

A typical mortgage payment is composed of four core components, commonly known by the acronym PITI. A clear understanding of each part is essential for sound financial management.

• Principal (P): The portion of the payment that directly reduces the outstanding loan balance. It is the repayment of the money originally borrowed.

• Interest (I): The lender's fee for providing the loan. This portion of the payment is the cost of borrowing and does not reduce the loan balance or build equity.

• Taxes (T): The portion of the payment that covers local and state property taxes. The lender collects this money monthly to ensure tax obligations are paid on time.

• Insurance (I): The portion that covers homeowners insurance, which protects the property from damage, and potentially Private Mortgage Insurance (PMI), which protects the lender if the borrower defaults on a loan with a down payment of less than 20%.

The tax and insurance components of the payment are typically managed through a lender-held savings vehicle called an escrow account. The borrower contributes one-twelfth of the estimated annual tax and insurance bills with each monthly payment, and the lender pays these bills on the borrower's behalf when they are due. This arrangement simplifies budgeting for the borrower and protects the lender's collateral. However, because property taxes and homeowners insurance premiums can change annually, the total monthly payment on a "fixed-rate" loan can fluctuate. This is a common source of payment shock for homeowners that is unrelated to the loan's interest rate.

Amortization is the process of paying off debt through regular installments. For a fixed-rate mortgage, the combined principal and interest payment remains constant, but the allocation between the two changes with every payment. In the early years of the loan, when the principal balance is highest, the vast majority of the payment is consumed by interest charges. For example, on a $400,000 30-year loan with a 6% interest rate, the first monthly principal and interest payment is $2,398.20. Of that amount, a full $2,000 is interest, and only $398.20 goes toward reducing the loan balance. This front-loaded interest means homeowners build equity very slowly at first. As the loan matures and the principal balance declines, a progressively larger share of each payment is applied to the principal, accelerating equity growth in the later years.

The Tale of Two Mortgages: Fixed-Rate vs. Adjustable-Rate

The most common type of home loan is the fixed-rate mortgage, which is defined by an interest rate that remains unchanged for the entire loan term, typically 15 or 30 years. This provides the borrower with a stable and predictable principal and interest payment, making long-term budgeting significantly easier. With a fixed-rate mortgage, the lender assumes the risk of future interest rate increases, as they are locked into receiving a lower rate of return if market rates rise. This stability is the primary advantage of a fixed-rate loan.

An adjustable-rate mortgage (ARM) is a loan with an interest rate that can change periodically. These loans typically begin with a lower "teaser" rate that is fixed for an initial period, such as five or seven years. After this period expires, the rate adjusts based on a simple formula: Interest Rate = Index + Margin. The index, such as the Secured Overnight Financing Rate (SOFR), reflects general market conditions and is beyond the lender's control. The margin is a fixed number of percentage points added by the lender that represents their profit. This structure is the mechanism for risk transfer: the fixed margin locks in the lender's profit, while the fluctuating index passes all market volatility directly to the borrower. To protect borrowers from extreme payment increases, ARMs include periodic and lifetime interest rate caps that limit how much the rate can change.

Specialized and historical mortgage products provide important context on the evolution of risk within the lending market. Interest-Only (I-O) ARMs required borrowers to pay only the accrued interest for an initial period, which resulted in very low initial payments. During this time, however, the principal balance did not decrease, meaning the borrower built no equity through payments. A significant payment shock occurred when the interest-only period ended and the loan was recalculated to fully amortize over the remaining term. Option ARMs, largely discontinued after 2014, offered a minimum payment option that was often insufficient to cover the interest due, leading to a dangerous condition known as negative amortization where the total amount owed grew over time even as the borrower made payments.

The Unseen Forces: What Drives Mortgage Rate Fluctuations?

A common misconception is that the Federal Reserve directly sets mortgage rates. In reality, the Fed's influence is powerful but mostly indirect. The Fed sets the federal funds rate, a very short-term rate that directly impacts variable-rate debt like ARMs and home equity lines of credit (HELOCs). However, the Fed's primary influence on long-term fixed mortgage rates comes from its policy statements, which shape investor expectations about the future health of the economy and inflation.

Inflation is a primary driver of mortgage rates. When inflation is high, the fixed payments a lender receives in the future are worth less in terms of purchasing power. To protect themselves from this erosion of value, lenders and investors demand a higher interest rate as compensation. This "inflation premium" is built into long-term loan rates, meaning periods of high inflation almost always lead to higher mortgage rates.

The most direct real-time indicator for the direction of 30-year fixed mortgage rates is the U.S. bond market, specifically the yield on the 10-year U.S. Treasury note. Most home loans are packaged and sold to investors as mortgage-backed securities (MBS), which compete with safe assets like Treasury bonds for investor capital. There is an inverse relationship between bond prices and their yields. When investor demand for bonds is high, prices rise and yields fall, which typically leads to lower mortgage rates. Conversely, when investors sell bonds, prices fall and yields rise, pushing mortgage rates higher. This market dynamic is forward-looking, meaning mortgage rates often move in anticipation of economic changes rather than just reacting to them.

The Bottom Line: Quantifying the Impact of Rate Changes

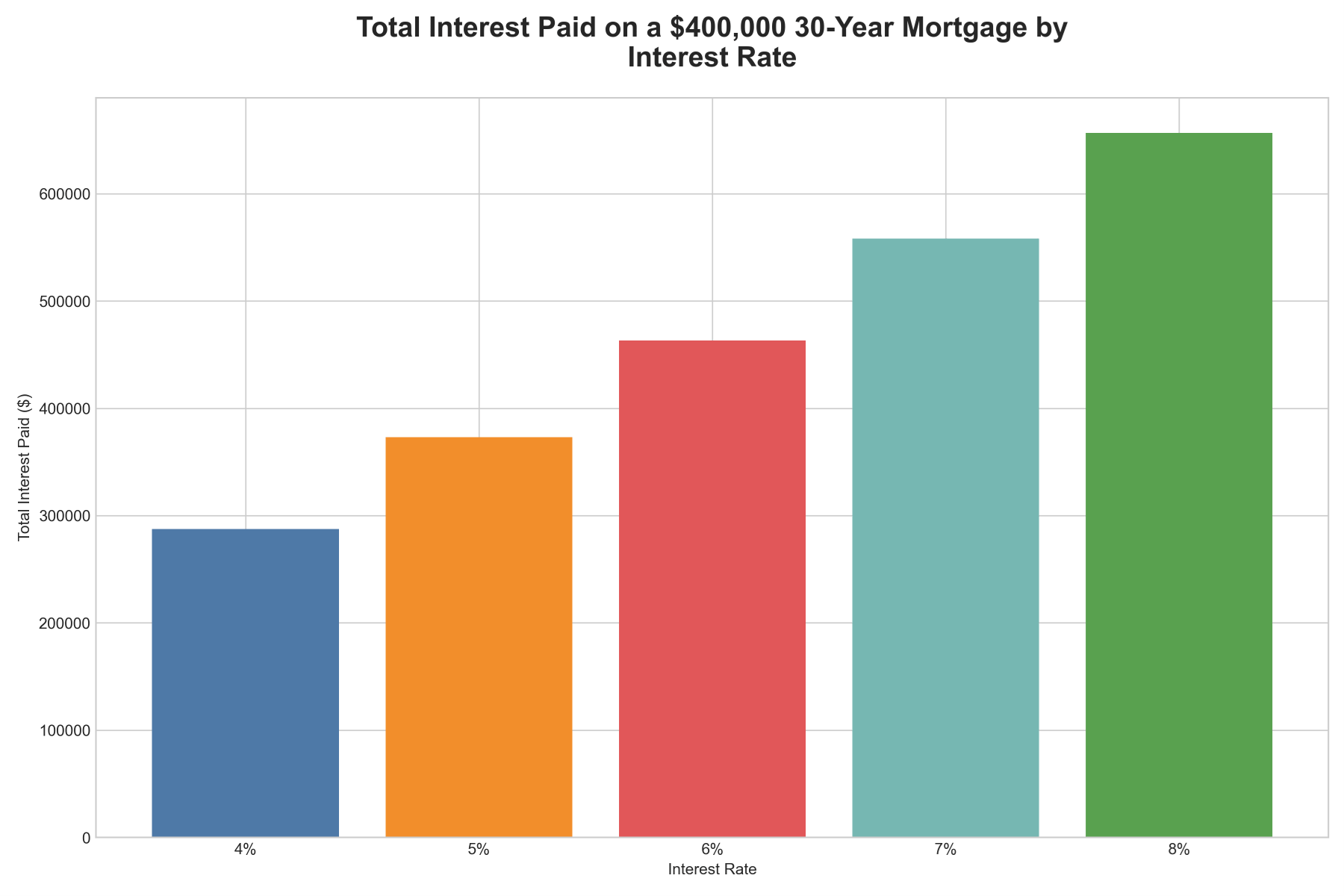

The long-term nature of a mortgage loan amplifies the effect of the interest rate. Even a minor change in the rate can result in a staggering difference in the total interest paid over the life of the loan. For example, on a $400,000 30-year loan, an increase in the interest rate from 6% to 7% increases the total interest paid by nearly $95,000. This illustrates the immense leverage that the interest rate exerts over the lifetime cost of borrowing.

Rising interest rates also directly diminish a homebuyer's purchasing power. Lenders qualify borrowers based on their debt-to-income (DTI) ratio. When rates rise, the monthly payment for any given loan amount increases. To keep the payment within DTI limits, a borrower must qualify for a smaller loan amount. A useful rule of thumb is that for every 1% increase in the mortgage rate, a buyer's purchasing power decreases by approximately 10%. For instance, a household that qualifies for a $500,000 mortgage at a 5% interest rate would likely only qualify for a $450,000 loan if the rate rose to 6%.

The impact of changing rates extends to the entire housing market. On one hand, rising rates cool demand by reducing affordability. On the other, they constrict supply because existing homeowners with low-rate mortgages are reluctant to sell. Giving up their favorable financing to buy a new home with a much higher rate creates a powerful "lock-in" effect that can severely limit the inventory of homes for sale. This can lead to a market where sales volume falls sharply, yet prices remain high due to a shortage of available properties.

Proactive Strategies for Homeowners

Homeowners have several proactive strategies for managing their mortgage in a changing rate environment.

Strategic refinancing, the process of replacing an existing mortgage with a new one, is a primary tool. The motivations include securing a lower interest rate, changing the loan term (e.g., from 30 years to 15 years to save on interest), or switching from an ARM to a fixed-rate loan for stability. A critical step in this process is calculating the break-even point: the time it takes for the monthly savings to cover the upfront closing costs of the new loan.

A more direct strategy is the prepayment of principal. By making extra payments applied directly to the loan balance, a homeowner can achieve significant interest savings, shorten the loan term by years, and accelerate equity growth. This can be done by making a lump-sum payment, adding a fixed extra amount to each monthly payment, or adopting a bi-weekly payment schedule that results in one extra full payment per year. This method does not require the costs or credit checks associated with refinancing.

Leveraging home equity through a Home Equity Line of Credit (HELOC) is another option. A HELOC functions as a revolving line of credit secured by the home. While it provides flexible access to funds, it also introduces risk. Most HELOCs have variable interest rates tied to benchmarks that follow Federal Reserve policy. In a rising-rate environment, the minimum payments on a HELOC can increase significantly, creating payment uncertainty.

Conclusion: Navigating Your Financial Future

To make timely financial decisions, homeowners and potential buyers should monitor several key forward-looking indicators. The most important real-time barometer for the direction of 30-year fixed mortgage rates is the 10-year U.S. Treasury yield. Its daily movements provide the clearest signal of where rates are heading. Inflation reports, such as the Consumer Price Index (CPI), are also critical, as they heavily influence both the bond market and Federal Reserve policy. Finally, official communications from the Federal Reserve offer crucial guidance on future monetary policy and shape the investor sentiment that ultimately drives mortgage rates.

A mortgage should not be viewed as a static, one-time transaction but as a dynamic, long-term financial instrument. Effective management requires a clear understanding of its structural mechanics, the macroeconomic forces that govern interest rates, and the strategic financial options available to the borrower. An informed and proactive approach is paramount to ensuring that a homeowner's largest liability is aligned with their long-term financial well-being.